This page includes relevant UK contents insurance statistics for 2024, such as:

- The evolution of the UK contents insurance market

- The impact on average UK contents insurance costs

- Contents insurance claims statistics outlining the most common claims made by customers

As of 2023, the average UK home contains almost £52,000 worth of contents. This means it’s important to work out exactly how much contents insurance cover you need in order to fully protect your personal possessions.

Our contents insurance report collates over 100 recent UK contents insurance statistics, alongside our own data, to analyse patterns and show how the market is changing. We can use this to compare contents insurance stats over time and suggest what the future might hold for UK customers.

Top 10 UK contents insurance statistics

- The average annual cost of UK contents insurance for Confused.com customers is £59.

- Nationally, the cost of contents insurance rose a third (33%) between 2015 and 2023.

- Choosing a £250 excess on your contents insurance policy could save you up to 11% a year compared to having £0 excess.

- Around 1 in 5 (22%) private renters don’t have contents insurance.

- Accidental damage is the most commonly cited reason for buying contents insurance (54%).

- Almost 4 in 5 (76%) contents insurance claims made in 2022 were successful.

- The average UK contents insurance payout in 2022 was almost £1,600. For Confused.com customers in 2022, this was £3,260.

- In 2022, there were more than 4.19 million UK contents insurance policies in existence, worth almost £437 million.

- More than a third (35.14%) of premiums in 2022 resulted in a payout.

- The most commonly insured items for Confused.com customers are laptops and cycles, representing 57% and 28% of respective contents insurance quotes during 2023-24.

Types of UK contents insurance

In the UK, there are 2 types of contents insurance:

- New-for-old insurance tends to cost more, but a payout should be enough to buy a brand new replacement.

- Indemnity insurance accounts for wear and tear of your belongings. For example, if a leak ruins your 3-year-old table, then a successful claim would likely pay out for you to buy another 3-year-old table.

Remember, contents insurance is different to buildings insurance. Buildings insurance covers the cost of repairing and rebuilding the structure of your home - the roof, ceilings, walls, and floor - but not the contents of your home.

There are also 3 main types of contents insurance policy available:

- Bedroom-rated - the insurer works out the amount of cover you need based on the number of bedrooms in your home. Typically, this provides between £40,000 and £50,000 worth of cover as standard, and is normally enough for the typical home. You should make sure this is enough to cover your personal possessions before agreeing to this type of policy though.

- Sum insured - You‘re responsible for calculating contents insurance and how much cover you need. The insurer doesn’t work this out for you. You can use an online contents calculator to work this out or you can do it yourself.

- Unlimited sum insured - This covers your contents without a limit so there’s no fear of being under-insured.

UK contents insurance cost statistics

What is the average cost of contents insurance?

According to our data between February 2023 February 2024, the average cost of UK contents insurance per year was £59 (or the equivalent of £1.13 per week). This is almost half the average amount reported by the ABI in February 2023 (£116).

We compare up to 76 home insurance providers across the UK to help you find our cheapest quote. You can claim a free reward when you buy contents insurance through Confused.com too.

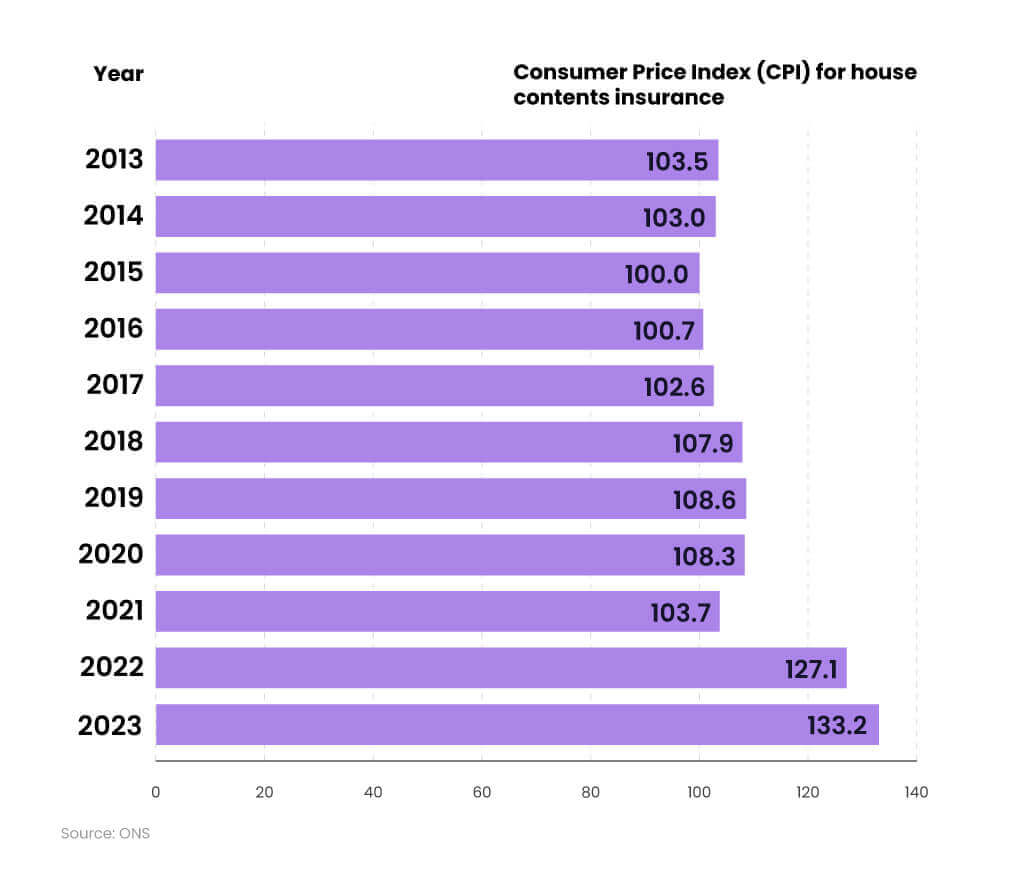

Consumer Price Index (CPI) statistics for house contents insurance

The Consumer Price Index (CPI) is used by the UK Government to judge the rate of inflation and track the cost of various items. As of 2023, the CPI for house contents insurance stood at 133.2, meaning that costs in this year were around a third (33%) more expensive than in 2015.

A breakdown of the annual Consumer Price Index (CPI) for house contents insurance between 2013 and 2023

Between 2015-22, there was a steady rise in the average cost of home insurance relative to 2015 figures, reaching a CPI of 108.3 in 2020.

During 2020-21, UK homeowners saw an average drop of 4.6% in their premiums, largely thanks to a reduced number of break-ins and cases of water damage during the Covid-19 lockdowns.

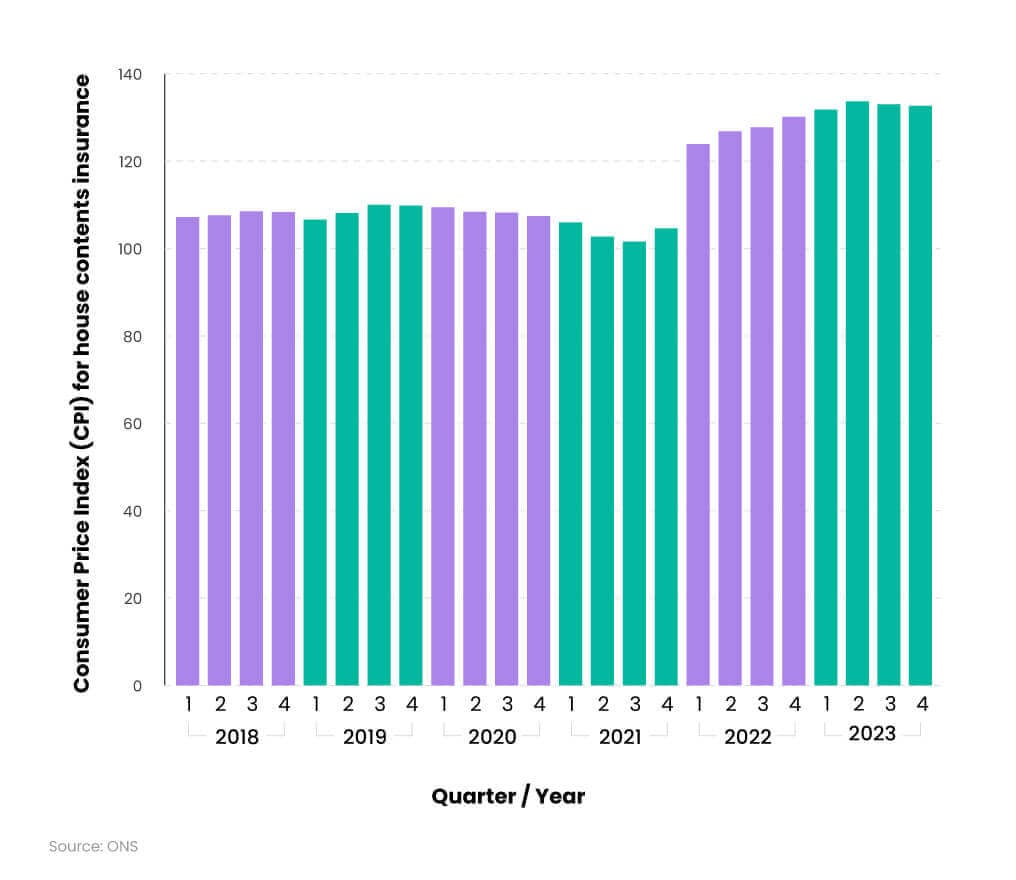

A breakdown of the quarterly Consumer Price Index (CPI) statistics for house contents insurance between 2018 and 2023

Since Q1 2022, the CPI for UK contents insurance has increased dramatically. At the start of the year the figure increased from 123.9 to 130.1 by Q4 2022, representing a rise of over 30% compared to 2015.

As of Q1 2023, the CPI for contents insurance stood at 131.8. This means consumers in this quarter were paying nearly a third (32%) more in 2023 than those in 2015.

The CPI for contents insurance peaked in the second quarter of 2023 at 134.4, marking a rise of more than a third (34%) compared to 2015. However, it slightly decreased in the third and fourth quarters, reaching 133.5 and 133.2, respectively.

A breakdown of the monthly Consumer Price Index (CPI) statistics for house contents insurance between 2022 and 2023

Since 2022, the CPI for UK contents insurance has dramatically increased, reaching a peak of 136.2 as of April 2023.

In May 2023, this dropped to 134.1. This meant the average UK contents insurance costs were more than a third (34.1%) higher compared to May 2015.

The CPI for contents insurance fell sharply in August 2023 to 113.4, the lowest level in the past two years. This narrowing gap means that, on average, UK contents insurance costs for 2023 were only 13% higher compared to 2015.

However, the CPI started to increase again in September 2023, settling at 132.6 by the end of that year.

What factors can affect the cost of UK contents insurance?

The cost of your contents insurance can be affected by:

- The value of your possessions. For example, you would need to name any high-value items over £1,000 on your main policy.

- Where you live.

- The type of home you live in.

- Your home’s security.

- Whether you rent or own your home.

- Who you live with.

- The risk of crime in the local area.

- Whether your home is in a flood risk area.

- Whether you work from home.

According to the ONS, almost 1 in 6 (16%) British workers worked from home between September 2022 and January 2023, with more than a quarter (28%) splitting their time between home and office.

Numerous factors can affect whether you’re covered to work from home by your contents insurance policy. These include:

- The type of work you do

- Who your employer is

- What equipment you’ll be using

For the majority of office/hybrid work, this should have little to no impact on your contents insurance. But, it’s worth checking with your employer and insurer to see what is and isn’t covered. For example, damage, loss, or theft of contents may not be covered under certain packages.

Are you living in a shared property with other people? If so, then you may want to look into shared house contents insurance to ensure your possessions are adequately covered against loss, theft, or damage.

Contents insurance statistics across the UK

Contents insurance is just one of the many different types of home insurance policies available across the UK.

According to our home insurance statistics, an estimated 7 million UK households are without home insurance. This means around a quarter of UK homes could be vulnerable should they fall victim to damage, destruction, or theft.

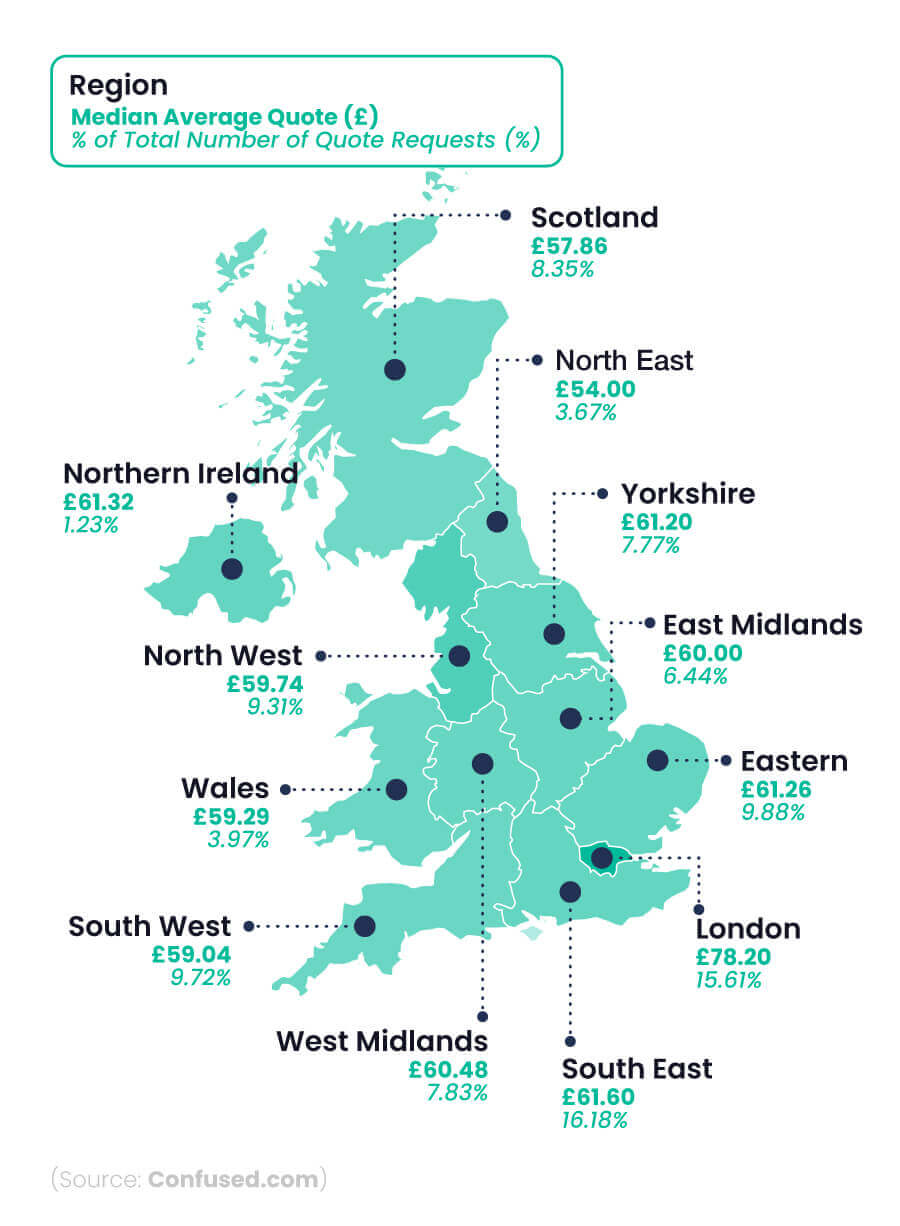

A breakdown of UK average contents insurance costs by region

When it comes to average cost, contents insurance coverage across the UK isn’t evenly distributed. For example:

- Residents in the North East of England tend to pay the least for their contents insurance, with an average cost of £54 per quote

- This is followed by households in Scotland and the South West of England, where the average cost of home insurance is between £57 and £59

On average, the most expensive regions in the UK for contents insurance between 2023-24 tend to be in London (£78.20) and the South East (£61.60).

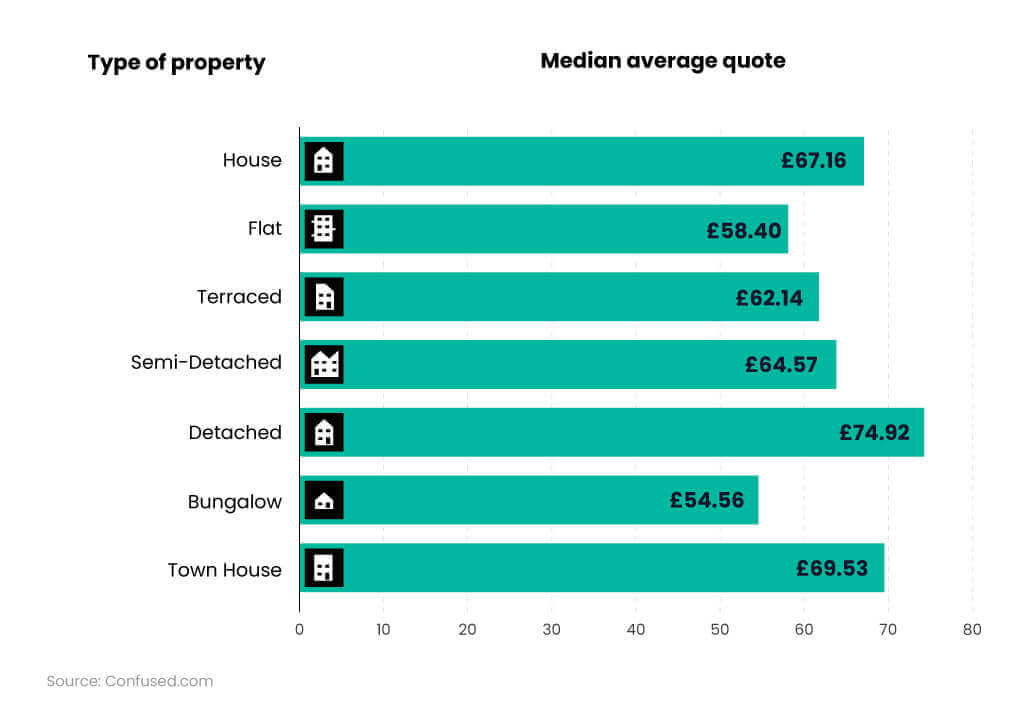

Average UK contents insurance costs by property type

If you rent a flat, the only type of flat insurance you need is contents. Your landlord should have buildings insurance in place to cover the cost of building repairs. That includes permanent fixtures too.

Between February 2023 and February 2024, the average price of contents insurance for someone living in a house was £67 for the year. But the price you end up paying can vary depending on the type of house you live in.

A breakdown of the average contents insurance costs in the UK by type of property

Based on quotes between February 2023 and February 2024, the average cost of contents insurance was cheapest for bungalows (£54.60), followed by:

- Flat (£58.40)

- Terraced (£62.14)

- Semi-detached (£64.57)

On average, the most expensive type of property for contents insurance was detached housing (£74.92). This is just over £5 a year more than the next most expensive option, a townhouse.

Average cost of contents insurance by number of bedrooms

The average cost of contents insurance tends to decrease along with the number of bedrooms in a property. For example, the price for a single-bedroom property was £52.92 on average between February 2023 and February 2024. This is more than double the savings compared to the average contents insurance for a typical UK property with 6 or more rooms, which is priced at £134.98.

A breakdown of average UK contents insurance costs by number of bedrooms

In terms of the number of bedrooms, 2 and 3 bedroom properties generated the most quotes between 2023-24. These accounted for around 7 in 10 (72.9%) quotes during this period.

The average contents insurance cost for 2-bed houses was around £58.07. This was almost £9 a year cheaper than the average contents insurance cost for 3-bed houses in the UK.

Average UK contents insurance costs by age group

Generally speaking, the average cost of contents insurance decreases as you get older. Between 2023-24, those aged 81 and over were quoted at £46.37 a year to insure their belongings. This was around a third (34.4%) less compared to those aged 26-30 (£65.70).

However, from the age of 21, average contents insurance costs tend to increase slightly year-on-year. For example, it increases from £64.81 to £72 for those aged between 41-45 years old.

A breakdown of average UK contents insurance costs by age

Between February 2023 and February 2024, those aged 17-20 were quoted the most for their contents insurance (£77.44). This is just over £30 a year more than those aged 81 and over

UK student contents insurance statistics

According to student cost of living statistics, almost two-thirds (59%) of UK students surveyed by Confused.com didn’t have contents insurance while at university. The 2023 survey reveals that more than half (52%) of those questioned didn’t know what contents insurance was when they went to university. Around two-fifths (40%) also admitted they didn’t know they needed contents insurance while away from home.

A typical student could easily have more than £3,000 worth of possessions when they head off to university. Therefore, buying adequate cover helps them to ensure protection against damage, theft, and destruction.

Students are a target group when it comes to criminals. According to Save The Student, around 1 in 20 (6%) students have been burgled or experienced a break-in while at university.

The ONS reported that 16.6% of all personal crime is reported by students. So not having contents insurance as a student could end up costing you more in the long run if you’re not suitably protected.

Some university halls may provide a basic level of student contents insurance. But, this may only include a limited range of items, and usually, they must be in your room at the time of a break-in, with windows and doors fully secured. Ensure you fully read and understand the terms and conditions of your policy before committing to it.

Average UK contents insurance costs by payment method

Paying for your contents insurance annually could help reduce the cost of your home insurance, with savings of up to 20%.

A breakdown of average UK contents insurance costs between annual and monthly payments.

| Payment method | % of total number of quote requests | Median average quote (£) |

|---|---|---|

|

Annual

|

69.09%

|

59.29

|

|

Monthly

|

30.91%

|

70.54

|

(Source: Confused.com)

As of 2024, the typical yearly cost for contents insurance among Confused.com customers was £59.29 and represented more than two-thirds (69%) of all quotes.

By comparison, the annual equivalent cost of paying monthly averaged £70.54 – almost a fifth (17%) more than those who chose to pay annually.

Get a contents insurance quote today to see how much you could save on your policy.

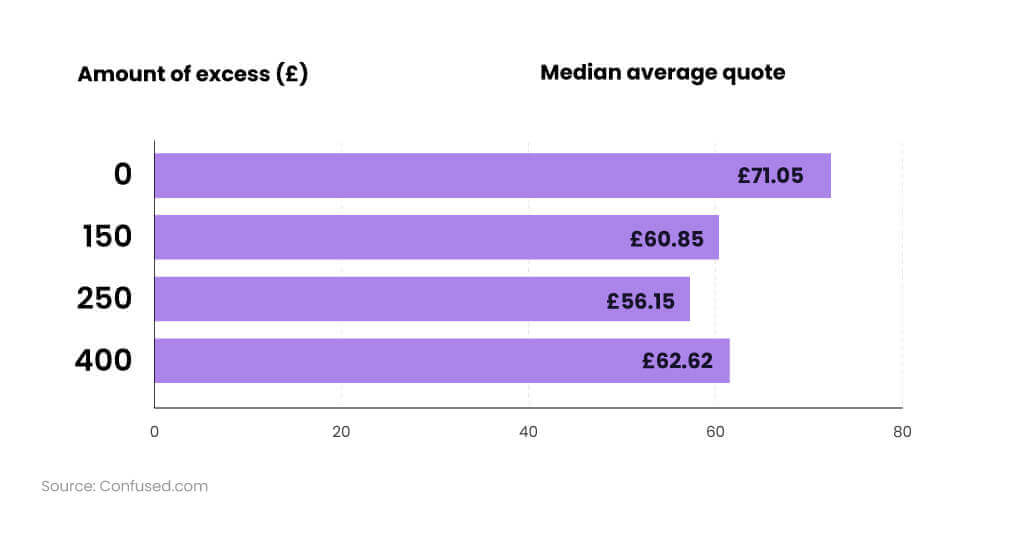

Average UK contents insurance costs by amount of excess

Another factor to consider is how much voluntary excess to pay. Based on Confused.com data between January and June 2023, a £250 voluntary excess could reduce your contents insurance costs by as much as 11%. This is compared to a similar policy with no excess.

But you need to pay this amount against any claim made on your home insurance.

A breakdown of UK average contents insurance costs by excess amount

Generally speaking, the more excess you select on your contents insurance, the cheaper it should be. That’s according to our quote data between 2023-24. For example, the average cost of a policy with £250 excess was £15 a year less compared to one with no excess (£71.05 vs £56.15).

But this figure increased for those who had a policy with £400 excess to £62.62 a year on average.

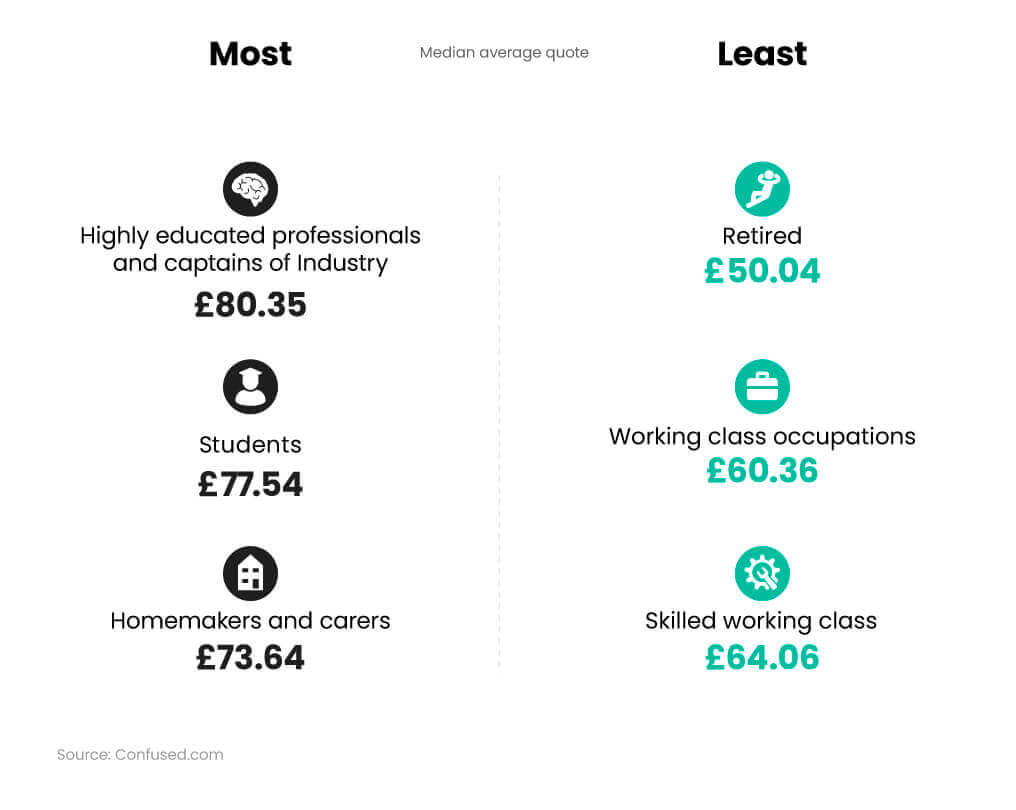

Average cost of contents insurance by occupational class

Contents insurance tends to be cheapest for those who are retired. If you’re retired, you can expect to pay around £50 for a typical contents insurance policy. Retirees accounted for nearly a quarter (24%) of our quotes in 2023-2024.

A breakdown of average contents insurance cost by employment status

At the other end of the scale, students faced some of the most expensive contents insurance quotes between 2023-24, averaging at £77.54. But this was the smallest represented group in our study, representing less than 2% of all quotes during this period.

Average cost of contents insurance by type of employment

On average, homemakers or those who are retired can expect to pay the least for their contents insurance (£52), followed closely by unskilled workers (59.37) and city drivers (£60.59).

The most expensive average costs of contents insurance tends to be for those working in:

- Entertainment (£78)

- Students (£77.69)

- Finance/Insurance (£74.53)

For these industries, the average price for contents insurance could be around £20 more than homemakers or those who are retired.

A breakdown of average contents insurance cost by type of work

The most popular industry represented in Confused.com contents insurance quote data between 2023-24 was housewives and retirees (27.04%). For these people, the average price of contents insurance was £52.

Average cost of contents insurance by total value of contents

Generally speaking, as the total value of your contents increases, so does the average cost of your contents insurance.

Between 2023 and 2024, around a fifth (20%) of Confused.com quotes were to insure items with a combined value of £20,000-£29,999. That makes it the most requested quote value during this period. This makes it one of the cheapest options for contents insurance, with an average quote of £56.67. The lowest price available starts at an average of £54.47 for coverage between £0 and £9,999.

A breakdown of average contents insurance cost by value of contents

Once the total value of your items starts going above £60,000, then the average cost of contents insurance increases to around £76.27 per year.

On average, someone who’s insuring items worth more than £120,000 can expect to pay anywhere between £145.36 and £293.55 for their annual policy. That’s almost 5 times more than those insuring £30,000 worth of contents.

Most common items insured on UK contents insurance policies

The 2 most common items that customers insure on their contents insurance are laptops (57.14%) and cycles (27.62%), in accordance with our very own quote data.

Between 2023-24, the average cost of contents insurance for laptops was around £800, while for cycles – bicycle insurance being one of the cheapest contents insurance policies – this figure dropped to an average of £700.

A breakdown of most commonly insured items on UK contents insurance

The most expensive policies tended to be for insuring items such as:

- Watches (£4,000)

- Jewllery (£3,000)

- Audio equipment (£2,100)

A breakdown of items that increase the average cost of contents insurance the most

| Item | % of total number of quote requests | Median average quote |

|---|---|---|

|

Item containing silver

|

0.19%

|

£223.89

|

|

Work of art

|

1.52%

|

£217.05

|

|

Watch

|

15.53%

|

£216.19

|

|

Containing precious stones

|

0.75%

|

£211.44

|

|

Clothing

|

0.95%

|

£210.89

|

|

Fur

|

0.04%

|

£202.24

|

|

Picture

|

1.30%

|

£202.15

|

|

Masonic regalia

|

0.01%

|

£198.80

|

|

Containing gold

|

0.50%

|

£198.63

|

|

Jewellery

|

40.44%

|

£195.81

|

(Source: Confused.com)

Overall, contents insurance policies covering items containing silver are the most expensive to insure. On average, these policies cost £223.89 between 2020 and 2023, almost £5 a year more than policies insuring works of art.

A breakdown of items that increase the average cost of contents insurance the least

| Item | % of total number of quote requests | Median average quote |

|---|---|---|

|

Television games consoles

|

0.20%

|

£143.31

|

|

PCs (inc accessories not laptops)

|

3.52%

|

£146.04

|

|

Angling equipment

|

0.46%

|

£147.00

|

|

Hearing aid

|

1.39%

|

£147.47

|

|

Portable television

|

0.02%

|

£149.27

|

|

Laptop computers

|

46.59%

|

£153.44

|

|

Portable audio equipment

|

0.13%

|

£153.71

|

|

Mobile phone

|

1.79%

|

£157.25

|

|

Stamp collection

|

0.20%

|

£160.97

|

|

Television

|

4.28%

|

£161.54

|

(Source: Confused.com)

Between 2020 and 2023, the cheapest contents insurance quotes were for policies insuring television games consoles (£143.31). These are closely followed by PCs (£146.04).

Angling equipment and hearing aids were also relatively cheap by comparison, with both types of contents insurance policy averaging at around £147 for the year.

Contents insurance statistics by type of home ownership

Average UK contents insurance costs by type of home ownership

The most common type of quote generated by Confused.com customers between 2020-23 was for an unfurnished, rented property from a private landlord. This represented almost 2 in 5 (39.42%) quotes during this period with a mid-range average price of £57.64.

A breakdown of average contents insurance costs by type of home ownership

| Type of home ownership | % of total number of quote requests | Median average quote |

|---|---|---|

|

Renting unfurnished from a private landlord

|

39.42%

|

£57.64

|

|

Mortgaged and occupied by you

|

20.96%

|

£57.65

|

|

Owned and occupied by you

|

12.78%

|

£49.87

|

|

Renting unfurnished from council

|

11.91%

|

£56.52

|

|

Housing association

|

9.15%

|

£56.34

|

|

Renting furnished from a private landlord

|

5.54%

|

£68.72

|

|

Renting furnished from council

|

0.24%

|

£57.69

|

(Source: Confused.com)

Between 2020 and 2023, the cheapest average contents insurance cost was for property that was owner occupied. At just under £50 for the year, nearly 13% of customers requested this across the 3-year period.

But those living in furnished, rental accommodation from a private landlord can expect to pay the most for their contents insurance. On average, this came out at £68.72, almost £20 a year more than the cheapest option.

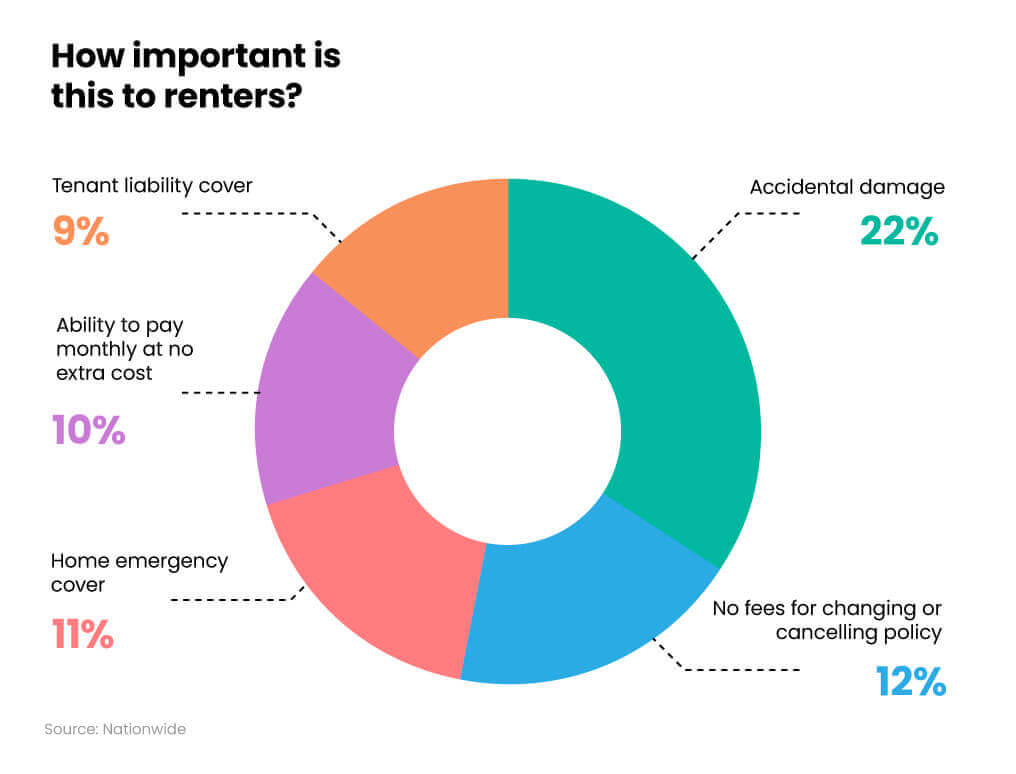

Contents insurance statistics for private renters

In a survey of more than 1,000 tenants, Nationwide Building Society found that half (52%) of the UK’s 4.4 million private renters had contents insurance. This leaves more than 2 million privately-rented households potentially unprotected against loss, theft, or damage to their possessions.

Nationwide’s study also found that:

- More than a fifth (22%) had no contents cover in place, with more than a quarter (26%) unsure if they had contents insurance or not.

- Almost 1 in 5 people wrongly believed it was the landlord’s responsibility to arrange contents insurance. Others didn’t get cover as a way of reducing monthly outgoings.

- Just under a half (48%) were worried that they might cause damage to their possessions in the future.

Separate landlords insurance is available for those who rent out properties to others. If the property is rented out furnished, then you may want to consider contents cover as a way to protect your items. Tenants insurance is also available for renters who wish to protect their personal belongings while renting.

Incidentally, accidental damage was the most commonly cited reason for private renters buying contents insurance (22%). That’s followed by no fees for changing/cancelling their policy (12%), and home emergency cover (10%).

A breakdown of how important different elements of home insurance are to private renters

The study also found that:

- Renters were paying for cover which they didn’t need. More than a quarter (26%) paid for buildings insurance, which is the landlord’s responsibility.

- Almost a third (32%) admitted to not cancelling their policy when they moved out of their rented accommodation.

- More than a third (34%) admitted to not knowing whether contents insurance was a requirement of their tenancy agreement.

- Almost 2 in 5 (39%) were ordered to arrange contents insurance by their landlord in 2021. And over two-thirds (67%) were asked for proof of contents insurance before they could sign their tenancy agreement.

UK contents insurance claims statistics

In 2022, 3% of UK insurance claims were for contents insurance. Insurers accepted over three-quarters (76.12%) of these claims, and the average payout was almost £1,600 per claim.

A breakdown of contents insurance claims statistics for the UK in 2022

| Claims frequency | 3.00% |

|---|---|

|

Claims acceptance rate

|

76.12%

|

|

Average claims payout

|

£1,573.77

|

|

Claim complaints as a % of claims

|

5.68%

|

|

Sum of average number of policies in force

|

4,196,679

|

|

Total retail premiums (written)

|

£437,495,107.00

|

|

% of premiums paid out in claims

|

35.14%

|

(Source: FCA)

In 2022, there were over 4.19 million contents insurance policies in the UK, costing more than £437 million. Insurers paid out more than a third (35.14%) of these premiums in claims.

Our guide on how to make a home insurance claim can give you more information on the claims process and whether it’s worth making a claim against your policy.

UK contents insurance claims statistics by type of claim

As home insurance isn’t mandatory, some may choose to save money and avoid buying it. But according to our research, the average contents insurance claim in 2022 was £3,260. If the average Confused.com customer pays £62 a year for their policy, it would take them 52 years to spend this amount without making a claim.

Between 2023 and 2024, the most common type of contents insurance claim was accidental loss caused by damage at home. More than half (54.02%) of quotes during this period were because of this and cost £108.93 on average.

A breakdown of contents insurance claims statistics by type of claim between 2023 and 2024

The next most common contents insurance claims during 2023-24 were accidental loss due to damage outside the home and theft outside the home, with average costs of £129.87 and £134.54, respectively.

Between 2023 and 2024, collisions were the main factor driving up insurance costs. These accounted for 0.06% of quotes during this period, with an average cost of £302.83.

Food stored in the freezer and water escape due to freezing resulted in average quote costs of less than £100 per year. Following that, the escape of water averaged at £85.68.

Subsidence and explosions are relatively uncommon in the realm of contents insurance claims, accounting for 0.04% of total quotes between 2023 and 2024.

In order to make a successful claim, it’s important to be honest and accurate with your insurer. Otherwise, you risk invalidating your house insurance and either receiving a partial payout or none at all.

Flood insurance claim statistics

A standalone flood insurance policy doesn’t exist in the world of home insurance because contents insurance policies should cover flooding as standard. Contents cover helps with the cost of repair, or replaces possessions if your home gets flooded.

Our data between May 2022 and May 2023 shows that the average cost of a claim for flood damage was £11,489.

The Environment Agency (EA) estimates that 1 in 6 properties in England are at risk of flood from rivers and seas, amounting to approximately 5.2 million homes. Also, the British Geological Survey (BGS) claims that up to 290,000 properties in England are also located in areas prone to risk from groundwater flooding.

Thankfully, since the launch of the Flood Re scheme in 2016, affordable home insurance with flood cover has now become a lot easier.

To be eligible for the scheme, your home insurance policy must be in your name, and your property must be:

- Built before 1 January 2019

- In a council tax band

- Used for residential purposes

Leasehold and residential buy-to-let properties should be covered by the scheme, providing they meet these criteria.

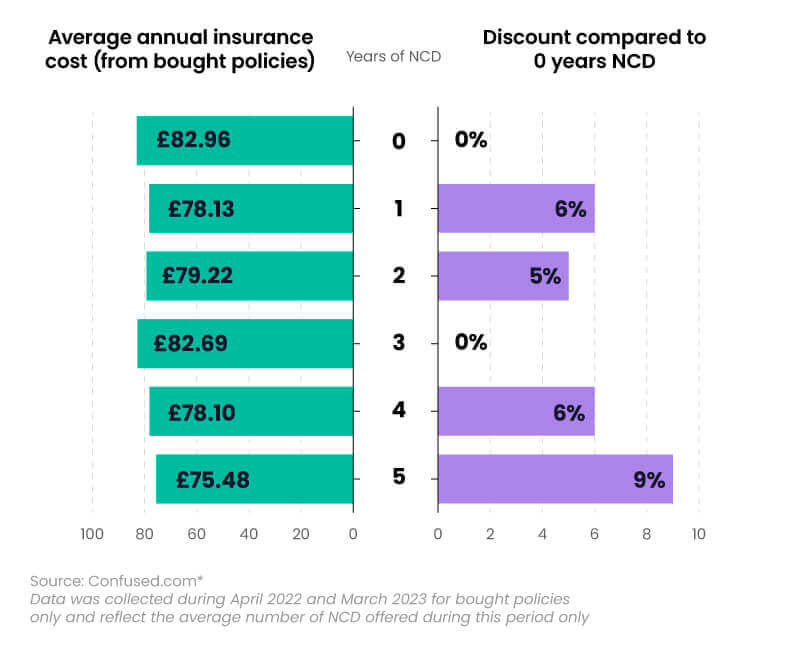

How does making a claim affect your contents insurance no-claims discount (NCD)?

Making a claim on your contents insurance policy may affect your no-claims discount (NCD), particularly when it comes to renewing your policy the following year.

A breakdown of average annual insurance costs for contents insurance and discount received for different levels of NCD

Our data between April 2022 and March 2023 shows that the average contents insurance policy with 0 years NCD was £82.69.

On average, customers saved the most with 5 years NCD (9%), followed by 1 year and 4 years (both 6%).

Contents insurance FAQs

What does contents insurance cover?

Contents insurance covers the cost of replacing or repairing your personal items if they’re destroyed, damaged, or stolen. This tends to include various household items that aren’t considered part of the structure or building. For example:

- Furniture

- Clothes

- Electronic equipment

- White goods

- Tools

- Jewellery

Is contents insurance mandatory?

No, contents insurance isn’t mandatory or a legal requirement. But having a contents insurance policy in place can help you protect your personal items against damage, destruction, or theft.

Do tenants need contents insurance?

No, tenants aren’t required to have contents insurance. But if their personal possessions become damaged, destroyed, or stolen, then the cost of repair or replacement won’t be covered. So it’s advisable to have a contents insurance policy in place, in order to protect these personal items.

How much contents insurance do I need?

The amount of contents insurance you need depends on the total cost of all your possessions. If you undervalue your contents, your insurer’s payout may not be enough to cover the cost of repair or replacement. If you overestimate the value of your items, then you could end up paying more than you need to for your contents insurance.

Is £50,000 enough for contents insurance?

As of 2023, the average UK home is estimated to contain around £52,000 worth of items. Therefore a contents insurance policy covering items up to the combined value of £50,000 might be enough. But this depends on how much your items are worth, and the repair or replacement cost if they get damaged, destroyed, or stolen. It’s important to accurately calculate the total value of your household items in order to get the most appropriate policy for you.

How much does contents insurance cost?

The cost of contents insurance varies depending factors such as:

- The value of your possessions

- Where you live

- The type of home you have

- Your home security

- Who you live with

- The risk of crime

- The risk of flooding in the local area

Between 2020-23, the cost of contents insurance ranged between £42 and £340 for the year.

What is the average cost of contents insurance?

Between February 2023 and February 2024, the average cost of contents insurance per month was £59. In February 2023, the ABI reported that the national average for contents insurance was £116.

How much is contents insurance per month?

Between 2023-24, the average cost of contents insurance was £5,88 per month (£70.54 annual equivalent). This is compared to £59.29 for an annual policy.

How much is contents insurance for renters in the UK?

Between 2020-23, contents insurance for renters in the UK ranged between £56.52 and £68.72. The amount depended on whether they were renting from the council or a private landlord, and whether the property was furnished or unfurnished.

How much is student contents insurance?

As of 2022, the average cost of student contents insurance was £59.15.

How much is contents insurance for a flat?

Between February 2023 and February 2024, average contents insurance for a flat was around £58 a year.

Is content insurance worth it?

In the unfortunate event that your personal possessions become damaged, destroyed, lost, or stolen, then having a contents insurance policy in place is definitely worth it. Otherwise, you’re faced with replacing them yourself, if they were to be lost, stolen, or damaged.

How soon can you claim on contents insurance?

Generally, there’s no rule on how long you have to wait before making a claim on your contents insurance policy. In theory, as soon as your policy is live, you should be able to make a claim. But it’s worth checking the terms and conditions of your policy before setting this up. You’re advised to contact your insurance provider as soon as the incident has happened. Some incidents (such as flooding) can get worse the longer you leave it.

Can you cancel contents insurance anytime?

Yes, you should be able to cancel your contents insurance policy at any time. There is usually a 14-day ‘cooling off’ period after initially buying your policy. But, in order to cancel your contents insurance policy, you may have to pay an admin fee, which can be up to £50 depending on your provider.

Contents insurance glossary

Bedroom rated contents insurance

Bedroom rated contents insurance is where the insurer works out the amount of content cover you require, also called the ‘sum insured’. It’s usually based on the number of bedrooms in your property.

Consumer Price Index (CPI)

The Consumer Price Index (CPI) measures the average change in the price paid by consumers for various goods and services in the UK over a given period of time.

Contents insurance

Contents insurance covers the loss, theft, or damage to items in your home that aren’t part of its structure. It covers the cost of replacing or repairing your possessions should they become destroyed, damaged, or stolen.

Home emergency cover

Home emergency cover helps with the cost for urgent repairs to the utilities in your property (i.e. water, gas, and electricity). It may also cover:

- Boilers and heating

- Plumbing and drainage

- Roof damage

- Electrical failures

- Broken windows,doors, and locks

- Lost keys

- Pest infestation

But, this could vary between providers, so it’s worth checking with your insurer to see what is and isn’t covered by your policy.

Indemnity insurance

Indemnity insurance accounts for wear and tear of your possessions. If your items become damaged or destroyed, it will replace like-for-like, rather than a brand new item.

New-for-old insurance

New-for-old insurance can replace items with a brand new version if they become damaged, destroyed, or stolen.

No-claims discount (NCD)

No-claims discount (NCD), or no-claims bonus (NCB), is a discount awarded to your insurance policy as a reward for not making a claim over the previous 12 months.

Personal possessions insurance

Personal possessions insurance should cover anything you own that’s worth £1,000 or less. This is usually an additional fee on top of your standard contents insurance policy. But it covers your items against theft or damage when you take them out of the house.

Students contents insurance

Students' insurance protects your personal belongings while at university and living away from home. This can be in private rented or student accommodation, as well as halls of residence on campus.

Sum insured contents insurance

Sum insured contents insurance is where you - not the insurer,- are responsible for calculating contents insurance and the amount of cover you need.

Unlimited sum insured contents insurance

Unlimited sum contents insurance is where all your contents are covered without limit, meaning you don’t need to calculate how much your possessions are worth.